About eighteen months ago we commissioned research on the supply of new residential developments in the Central London property market.

The problem was that, while it was obvious from the acres of advertising in the property pages of every newspaper that there was plenty of supply coming down the line, information on the actual amount was thin on the ground.

Estate agents’ research departments were understandably coy on the matter as their developer clients would not be over the moon to have any perceived oversupply highlighted.

The objective, as far as we were concerned, was to shed some light, aiming to be roughly right – rather than precisely wrong.

Information was always going to be imperfect as getting accurate intelligence on sales from developers was not a realistic proposition. Equally, there would be dozens of different definitions of the words ‘Prime’, ‘Central’ and ‘London’.

We worked with Dataloft, our research company, and set about the analysis as follows.

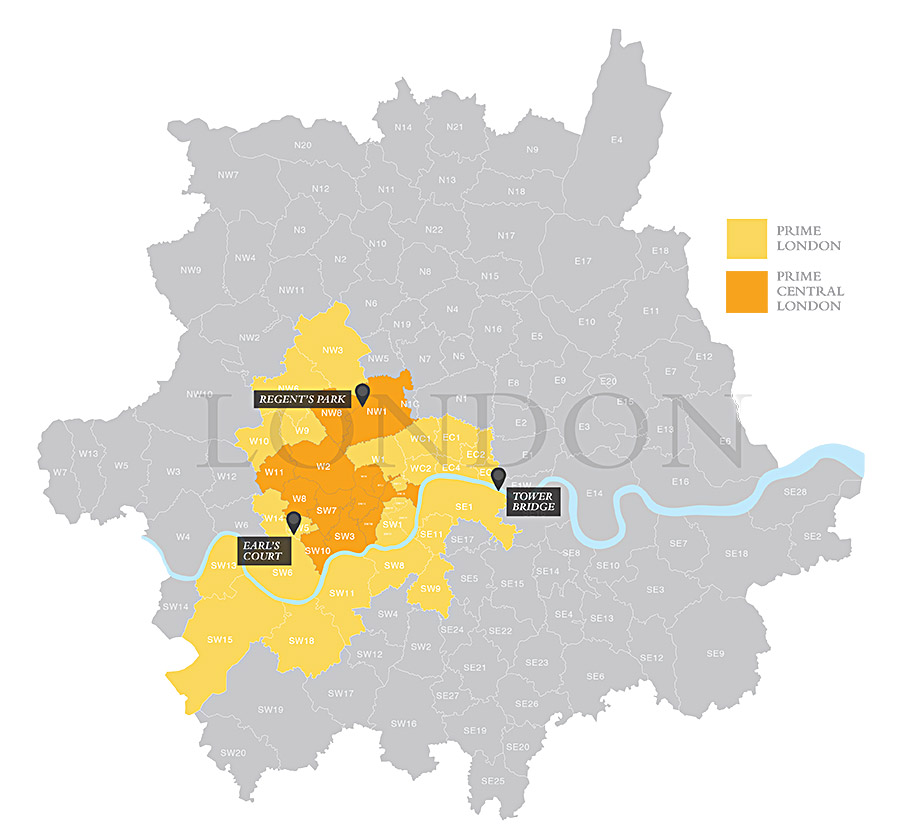

The ‘London’ that we are researching is divided into two: ‘Prime London’ and ‘Prime Central London’ and organized by postcode.

In very rough terms ‘Prime London’ goes as far west as Earl’s Court, as far north as Regent’s Park, as far east as Tower Bridge and includes the South Bank of the Thames.

The ‘Prime Central London’ area includes Mayfair, Marylebone (W1J&K) Knightsbridge, Belgravia, St James’s (SWIA&W&X), Chelsea (SW3), South Kensington (SW7) and West Chelsea (SW10). It also includes Notting Hill (W11), Kensington (W8) and Bayswater (W2) as well as St Johns Wood (NW1) and Regent’s Park (NW8).

The research is taken from publicly available planning information and is divided into three parts:

- Developments that are in the planning process – but do not yet have planning permission.

- Schemes with planning permission but which are not yet underway.

- Schemes under construction.

It does not include any development with under five units – which will under-report what is going on in the ‘Prime Central London’ area as the capacity there for large projects is limited and many will take the form of converting older houses.

It should also be noted that the definition of ‘Prime London’ excludes anything in Docklands or Wimbledon – which again will under-report the size of the wider development pipeline.

It needs to be emphasized, however, that getting planning permission does not necessarily mean that a project will be built out. We have heard of a number of schemes that have been mothballed or reconceived as offices: the shortage of office space (caused by residential conversions) has resulted in rents skyrocketing along with capital values.

As previously mentioned, it is also difficult to know what has already been sold – so it would be wise to make some conservative assumptions.

First, the raw data. If all the units within our definition of ‘Prime London’ and ‘Prime Central London’ achieve planning permission and get built, there will be 54,360 new units over the next few years. This figure hasn’t changed much in 18 months.

In the wider ‘Prime London’, which accounts for 47,877 units;

- 10% are in the application stage (4,788)

- 54% have planning permission (25,853)

- 36% are under construction (17,236)

In ‘Prime Central London’, which consists of 6,482 units, the split between planning application and construction is broadly the same, with:

- 17% in the planning process (1,102)

- 53% with permission (3,436)

- 30% under construction (1,944)

These are big numbers. In order to try and make it as conservative as possible we have applied the following assumptions:

- A third of the planning applications fail to get permission.

- A third of those with planning permission don’t get built.

- A third of the remainder with planning or under construction are already sold.

The figures would then be 26,133 for ‘Prime London’ and 3,565 for ‘Prime Central London’.

Are these still big numbers? The Land Registry has supplied data for what was sold last year in broadly the second-hand market at over a unit price of £700k.

We say broadly because their figures are for properties that have actually completed: they won’t include purchases of a new build where the buyer is paying by installments, or where such a purchaser sells on their contract.

It also has to be said that 2015 was a pretty dismal year for the London market which was hit by an election, SDLT increases, changes to Non-Dom status, Enveloped Property Taxation and the Mortgage Market Review.

However, none of these are going away soon and it is as good a snapshot of the second-hand market as we are going to get.

The actual numbers for the second-hand market are 2,151 for ‘Prime Central London’ and 4,870 for ‘Prime London’. The gap between the pipeline of new stock and the annual second-hand market in the wider area is large – very large.

So, what conclusion should you draw from this? Certainly not that the whole market is under a cloud of oversupply. If you go out and try to buy a nice 2/3 bedroom flat in Chelsea or South Kensington you won’t find much to look at; this remains a tightly held market with mainly discretionary sellers.

In the big regeneration areas it is another matter – and you will have to buy the very best – or very cheaply – to make a success of it. And there are some excellent schemes out there – alongside some that are truly awful.

The word ‘Prime’ has become overused in recent years, alongside ‘iconic’. As the market adjusts, their real meaning will become apparent and those who believed the developers’ hyperbole may wish they had taken more time – and advice.